Choosing between a Fixed vs Variable Mortgage is one of the most important financial decisions when buying a home. Your choice can affect your monthly payments, long-term interest costs, and overall financial stability. Understanding how each option works helps you make a confident and informed decision.

In this guide, we will break down the differences, advantages, risks, and ideal scenarios for both mortgage types. Whether you are a first-time buyer or refinancing your property, this article will help you choose the right path.

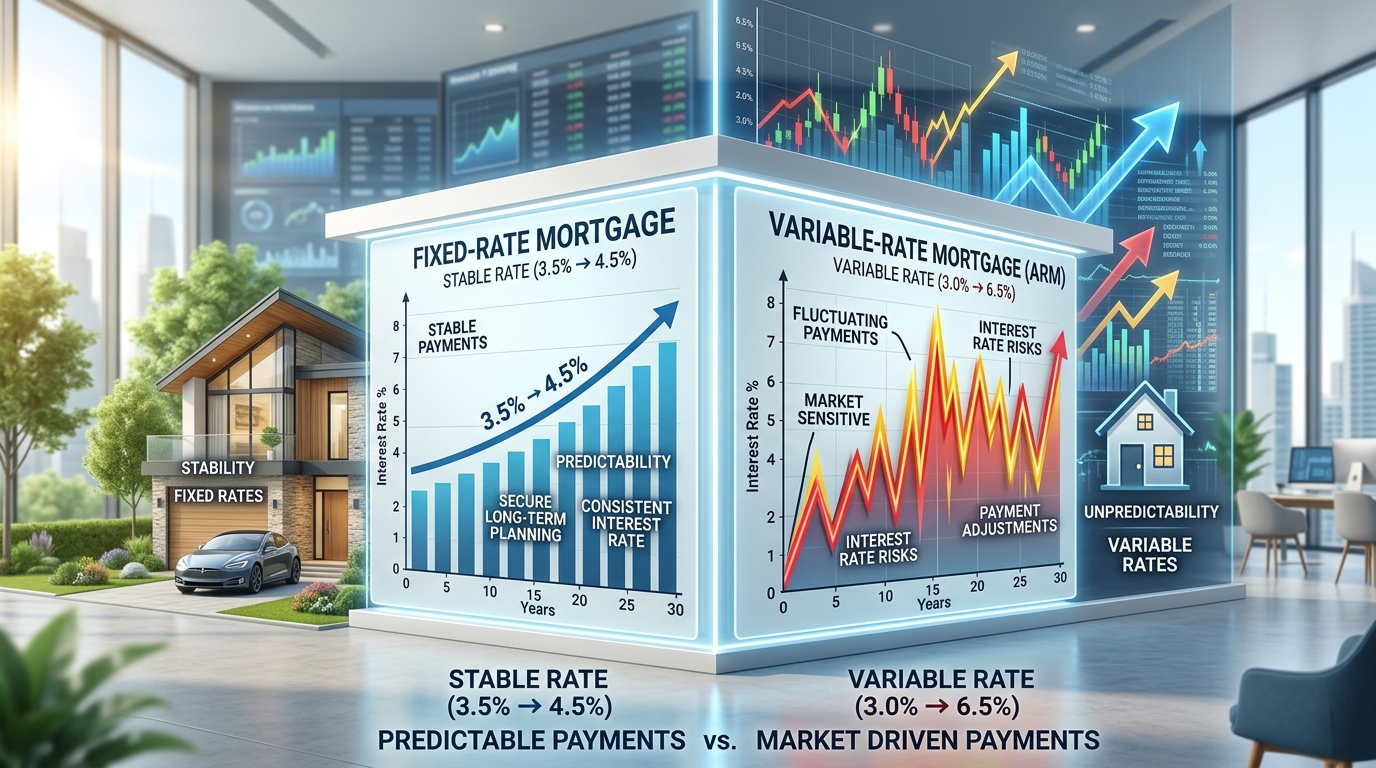

What Is a Fixed Rate Mortgage?

A fixed rate mortgage is a home loan where the interest rate stays the same throughout the loan term. This means your monthly payments remain consistent, regardless of changes in the market interest rates.

This type of mortgage is popular among buyers who prefer stability and long-term planning. You always know exactly how much you will pay each month, making budgeting easier.

Learn more about mortgage basics from Consumer Financial Protection Bureau.

Advantages of Fixed Rate Mortgages

Fixed mortgages offer several benefits:

- Predictable monthly payments

- Protection from rising interest rates

- Easy budgeting for long-term financial planning

For people who value stability over risk, fixed loans are often the preferred option in the online business-like financial world, where predictability is key to success.

Disadvantages of Fixed Rate Mortgages

However, fixed mortgages also come with limitations:

- Higher initial interest rates compared to variable loans

- Less flexibility if market rates drop

- Potentially higher long-term costs in certain conditions

What Is a Variable Rate Mortgage?

A variable rate mortgage, also known as an adjustable-rate mortgage, has an interest rate that changes over time based on market conditions. This means your monthly payments can go up or down.

Variable mortgages are often tied to a benchmark rate set by financial institutions or central banks. When these rates change, your loan repayment adjusts accordingly.

For updated interest rate trends, you can check Bank of England Monetary Policy.

Advantages of Variable Rate Mortgages

Variable mortgages offer several attractive benefits:

- Lower initial interest rates

- Potential savings when market rates drop

- More flexibility in certain loan structures

This structure can be appealing for borrowers who are comfortable with risk, similar to strategies used in affiliate marketing or dropshipping business models, where rewards can fluctuate based on market performance.

Disadvantages of Variable Rate Mortgages

However, the risks are important to consider:

- Unpredictable monthly payments

- Higher costs if interest rates rise

- Financial uncertainty for long-term planning

Fixed vs Variable Mortgage: Key Differences

Understanding the core differences between a Fixed vs Variable Mortgage helps you evaluate which suits your financial goals better.

| Feature | Fixed Mortgage | Variable Mortgage |

|---|---|---|

| Interest Rate | Constant | Changes with market |

| Monthly Payments | Stable | Fluctuating |

| Risk Level | Low | Medium to High |

| Best For | Long-term stability seekers | Risk-tolerant borrowers |

Which Mortgage Is Right for You?

There is no universal answer to choosing between a fixed and variable mortgage. Your decision depends on your financial situation, risk tolerance, and future plans.

Choose a Fixed Mortgage If:

- You prefer predictable expenses

- You are planning long-term homeownership

- You want protection from interest rate increases

Choose a Variable Mortgage If:

- You can handle financial fluctuations

- You expect interest rates to remain stable or decrease

- You want potentially lower initial payments

Think of it like choosing between a stable passive income stream versus a more dynamic income model. Stability reduces stress, but flexibility can sometimes lead to greater savings.

Factors to Consider Before Choosing

Before deciding on a Fixed vs Variable Mortgage, evaluate the following factors:

1. Current Market Conditions

Interest rate trends play a major role in determining which mortgage is more beneficial at the moment.

2. Income Stability

If your income is stable, you may handle a variable mortgage more easily. If not, fixed rates offer better protection.

3. Long-Term Financial Goals

Think about how long you plan to stay in the property and your future financial commitments.

4. Risk Tolerance

Some people prefer certainty, while others are comfortable taking calculated financial risks.

Common Mistakes Homebuyers Make

Many buyers rush their decision without proper research. Here are common mistakes to avoid:

- Choosing based only on the lowest initial rate

- Ignoring long-term interest rate trends

- Not considering personal financial stability

Making informed decisions is essential, just like in affiliate marketing or building an online business, where strategy matters more than short-term gains.

Fixed vs Variable Mortgage in Today’s Market

In today’s economic environment, both mortgage types have their place. Rising interest rates often make fixed mortgages more attractive, while stable or falling rates can favor variable options.

The key is to stay updated with financial trends and consult reliable sources or mortgage advisors before committing.

You can explore additional financial insights at Investopedia Mortgage Guide.

Final Thoughts

Choosing between a Fixed vs Variable Mortgage depends entirely on your financial goals and comfort with risk. Fixed mortgages offer stability and peace of mind, while variable mortgages offer flexibility and potential savings.

There is no one-size-fits-all solution. The best choice is the one that aligns with your income stability, long-term plans, and financial mindset.

Take your time, compare options, and consult a financial expert if needed. A well-informed decision today can save you thousands in the future.